Bankruptcy FAQ’s

![]()

WHAT IS BANKRUPTCY

Bankruptcy is one way of dealing with debts you cannot pay. Bankruptcy proceedings free you from overwhelming debts so you can make a fresh start, subject to some restrictions; and make sure your assets are shared out fairly among your creditors. Bankruptcy normally lasts for 3 years.

The role of the Insolvency Service of Ireland (ISI) is to restore insolvent debtors to solvency in a fair, transparent and equitable way.

Bankruptcy proceedings are brought in the High Court. When the person’s property is sold, the Official Assignee (ISI) will make sure that the proceeds are shared out fairly among creditors and any outstanding debt will be written off

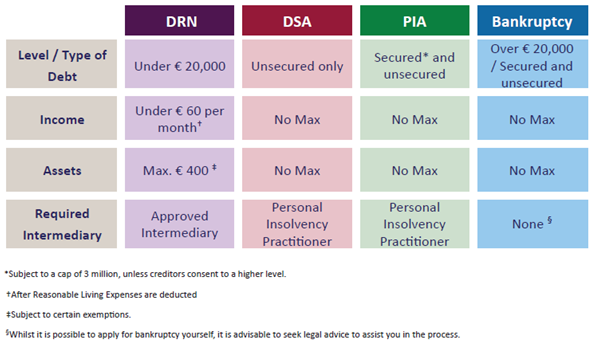

ALTERNATIVES TO BANKRUPTCY

MAIN CONSEQUENCES OF BANKRUPTCY

You: Debt Free, have a duty to contribute surplus income to the Official Assignee for 5 years

Official Assignee: Owns your assets, receives creditor claims, administers your estate, distributes payments to creditors

Creditor: Deal directly with Official Assignee and no longer contact you directly

WHO IS ELIGIBLE TO SEEK BANKRUPTCY

WHO IS ELIGIBLE TO SEEK BANKRUPTCY

-You are insolvent

-Must lodge €650 with Bankruptcy Division of the ISI

-You must swear an Affidavit stating that you have made reasonable efforts to make use of the alternative arrangements to bankruptcy such as DSA or PIA to the extent your financial circumstances permit you to.

-You must present a Statement of Affairs which will set out your financial situation and must disclose that your debts exceed your assets by more than €20,000.

-You must prepare a Petition for bankruptcy in which you must: (i)undertake to attend in person at the Statutory Sitting in Court, (ii)undertake to advertise notice of your bankruptcy adjudication and Statutory Sitting, and (iii) make various statements regarding your Centre of Main Interest (COMI), domicile or related matters.

WHAT TYPE OF DEBT CAN OR CANNOT BE INCLUDED IN BANKRUPTCY

|

Can |

May | Can’t |

| -Personal Loans-Business/commercial loans-Family maintenance payments under court orders-Revenue Debt

-Personal Guarantees -Unsecured portion of property loans -Trade Debts |

-Secured debt (eg mortgage) |

-Court fines in respect of criminal offences-Debts incurred after date of bankruptcy declaration |

DUTIES AND OBLIGATIONS:

-You must attend court on the day your bankruptcy application is listed AND on the day of the Statutory Court Sitting

-Full co-operation with the Official Assignee in all matters regarding your bankruptcy

-You must attend the Bankruptcy Division of the ISI to be served with a Bankruptcy Order and a Warrant of Seizure, usually on the day you are made bankrupt. Ownership of all your property will automatically transfer to the Official Assignee.

-Called for an interview with the Official Assignee having completed a Statement of Personal Info and Statement of Affairs in relation to your estate

-You must publish the date of your court sitting in Iris Oifigiúil and a national daily newspaper

-Legal obligations with administration with your account: delivery of accounts/documents when requested, delivery of title deeds, assisting the Official Assignee with your estate administration, disclosing property acquired since date of bankruptcy

-Inform the Assignee if you change your address

HOW WILL BANKRUPTCY AFFECT YOU

You can continue in current employment or seek new employment while you are bankrupt. If in employment the Official Assignee will seek a contribution from your income after applying the ISI Guidelines on Reasonable Living Expenses

You can still trade if you are bankrupt if and only if you trade in the same name in which you were made bankrupt. When a partner is adjudicated bankrupt, the partnership is automatically dissolved unless the partnership agreement provides otherwise.

Your pension assets are not transferred to the Official Assignee but pension income receivable by you will be treated as income for the purposes of your bankruptcy.

The bankrupt person’s interest or share in the family home transfers to the Official Assignee as with all other property. You may not necessarily lose your family home in bankruptcy. You may be able to agree a schedule of mortgage payments with your bank and the Official Assignee, where such payments are within the Reasonable Living Expenses approved by him

In reference to property abroad, under the European Community Insolvency Regulation, bankruptcy proceedings in Ireland may be recogniSed as insolvency proceedings in all European Community Member States (except Denmark), where the centre of main interest (COMI) of the bankrupt person is within Ireland

The Official Assignee can review, and possibly challenge, any property transfers made before bankruptcy.

The only assets that do not transfer to the Official Assignee are essential assets up to a value of € 6,000 (including vehicles), or more, if the High Court allows

If you obtain credit of € 650 or more without disclosing your bankruptcy, you are guilty of an offence under the Bankruptcy Act, 1988 as amended

There is no outright prohibition on you travelling abroad but you should inform the Official Assignee if you intend to do so.

Your financial circumstances will be reviewed on a 6 monthly basis throughout your bankruptcy and you will be obliged to complete an income and expenses form to assist in the assessment at each review

Your name will not be removed from the Bankruptcy Register. It is a register of all bankruptcies, including those that have been discharged.

How long does bankruptcy last?You will normally be automatically discharged from bankruptcy after 3 years. This period could be shorter if you can come to a settlement with your creditors

![]()

AJ Debt Solutions

(01)5352965 | info@debtsolutions.ie| 30 Francis St, D8

admin

© Copyright 2016. Anthony Joyce is authorised by the Insolvency Service of Ireland to carry on practice as a personal insolvency practitioner.